How Does the Collections Process Work?

Let's Follow an Account Through

the Collections Process

What happens to an overdue account once it's sent to collections?

That may depend on the type of debt incurred. Credit card debts, medical debts, and student loan debts are the most common types of debt sent to collections, although car loans, utility bills, personal loans, and cell phone bills are also quite prevalent.

Assigned or Sold?

Creditors may either

assign the debt to a collector, or they may

sell it. Assigned debts are still owned by the creditor, and the collection agency takes its cues from him. For example, with an assigned debt, the collector cannot negotiate a settlement or pursue legal action without the creditor’s authorization.

If a debt is purchased outright by a collection agency, the creditor no longer has any responsibility for the overdue account.

Almost all debt collectors work on assigned debts for a contingency fee. That is, they are paid with a percentage of the total amount collected. Usually, higher percentages are paid for older accounts.

The Collections Process

Debt collectors first use letters and phone calls in their attempt to contact consumers. The purpose of this is twofold: To verify the consumer's identity and to persuade the consumer to pay his debt.

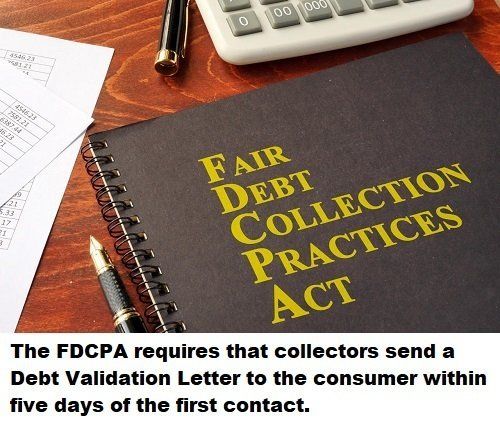

Within five days of this first contact with the consumer, the collector must issue a Debt Validation Letter. This letter is required by the Fair Debt Collection Practices Act (FDCPA).

The Debt Validation Letter must include the following:

- The total amount of the debt.

- The name of the creditor seeking payment.

- A statement indicating that, unless the consumer disputes the debt within 30 days of the first contact, the collector assumes the debt to be valid.

- A statement indicating that the collector will verify the debt by mail if the consumer writes to dispute the debt or request more information within 30 days.

- A statement indicating that, if requested, the collector will provide the consumer with information about the original creditor within 30 days.

If the consumer requests debt verification, collection activities are suspended while the debt is being verified and the Debt Verification Letter is being prepared.

Thereafter, the regular schedule of collection letters and phone calls may be resumed. In all communications, the collector should respectfully request payment and explain the time frame for reporting delinquencies to the credit bureaus.

This schedule of letters and phone calls continues until a payment agreement is reached. At this point, if all attempts to collect the debt have been unsuccessful, the creditor may authorize legal recourse.

When Legal Action Is Necessary

Once a debt is very delinquent (e.g., 120 or 180 days overdue) and resolution does not appear likely, the collector may choose to pursue legal action, with the creditor’s approval. A debt collector may also pursue legal action if the debt is nearing its statute of limitations.

(See sidebar below.)

The Statute of Limitations

The statute of limitations on debt varies from state to state and is categorized according to four types of debt:

- Oral agreements

- Written contracts

- Promissory notes

- Open-ended accounts

Once the statute of limitations has run on a debt, legal action may no longer be pursued.

However, collectors may still pursue recovery on these time-barred debts, so long as they comply with the FDCPA. In addition, if the consumer asks about the statute of limitations, the collector must explain that the debt is time-barred.

Please note that resolution is still attempted

throughout this legal process,

allowing the consumer every opportunity to

resolve the debt.

If the lawsuit is valid, a judgment will be issued by the court, ordering the consumer to pay the debt. Without this court order, the debt collector cannot seize a consumer’s bank account or paycheck. But with a judgment, the collector is authorized to perform certain actions in order to recover payment.

Typically, those actions would involve one or more of the following:

- Garnishing a percentage of the consumer’s wages through a garnishment order, for 120 days or until the debt is paid in full. The percentage garnished is based on the consumer's income and does not drain the paycheck.

- Placing a levy on the consumer's bank account or vehicle, allowing the creditor to seize the asset.

- Placing a lien on the consumer's property.

- Forcing the sale of an asset in order to pay the debt.

Of these options, wage garnishment is the most common action taken. It is also the only action that CBSI currently takes to resolve the debt legally. The other options, while legally available, are not very consumer-friendly.

Garnishing a portion of the consumer's paycheck is effective without jeopardizing the customer relationship, as the judgment does not indicate the client company name.

At CBSI, our collection professionals treat both our clients and their consumers with respect and dignity throughout the entire collections process. We're passionate about compliance and client satisfaction, and our recovery rate is one of the highest in the industry.

Recent Posts

Share On: