The Personality of Debt

How Personality Impacts

Financial Health

Our unique personalities shape our spending and saving habits, impacting our financial health.

Although personality alone does not determine financial behavior, it does significantly influence the way individuals manage their money. For instance, research studies have identified a definitive connection between certain character traits and the probability of accumulating debt.

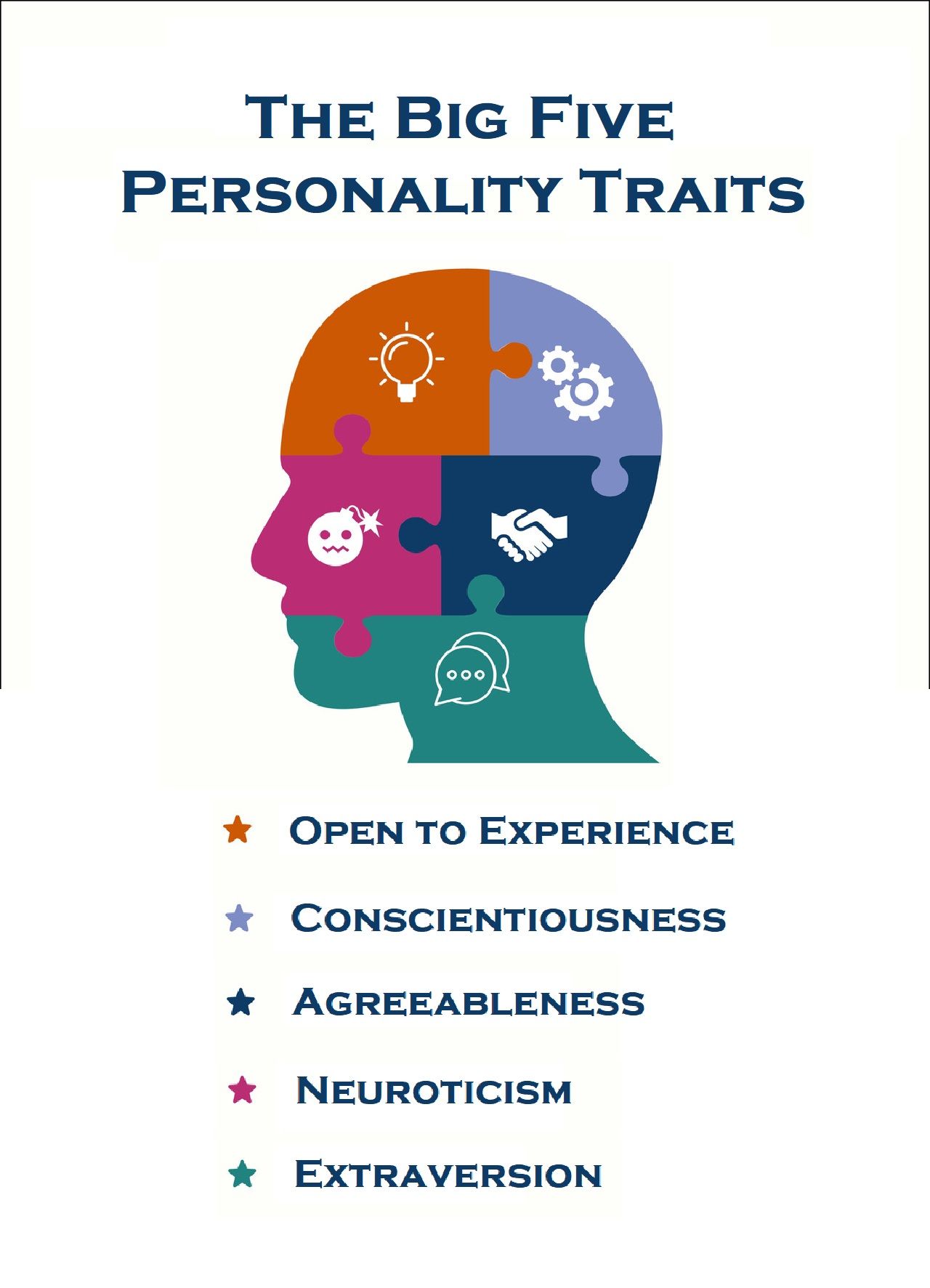

Mapping Personality Traits

When correlating personality traits with financial health, most psychologists employ a widely accepted model known as the “Big Five.” This method describes personality in terms of five broad dimensions: Openness, Conscientiousness, Agreeableness, Neuroticism, and Extraversion. Each of us possesses a unique combination of these traits, influencing our behavior and reactions to various situations.

These traits exist on a spectrum, and individuals differ in the degree to which they express each one. For example, a person may be very extraverted, somewhat extraverted, or not at all extraverted.

Linking Personality Traits and Debt

For each of the Big Five, there is a definitive correlation between the individual trait and the likelihood of accumulating debt:

Openness

Openness to experience is associated with creativity, curiosity, and a willingness to explore new ideas and perspectives. Some studies suggest that individuals with high levels of openness are more willing to assume debt for novel experiences or to invest in personal growth.

Conscientiousness

This personality trait is associated with responsibility, organization, and a desire to achieve goals. Research indicates that individuals with high levels of conscientiousness tend to be better at budgeting, planning for the future, and controlling their spending habits, making them less likely to accumulate debt. On the other hand, people with very low levels of conscientiousness tend to be impulsive, acting without considering the consequences. Such consumers are often driven by a desire for immediate gratification and struggle with self-control when it comes to spending.

--Article Continues Below--

Agreeableness

Agreeableness as a personality trait is associated with cooperation and kindness. However, one of the few drawbacks to this trait is in the domain of personal finances. Highly agreeable people tend to perform worse on various key financial metrics, including lower savings balances, lower incomes, and greater economic hardship (e.g., debts, insolvency). Agreeable people may also be more easily manipulated into making irresponsible spending decisions.

Neuroticism

Neuroticism is characterized by emotional instability, anxiety, and a tendency toward negative perceptions. Individuals with high levels of neuroticism may use spending as a coping mechanism to deal with stress and painful emotions. They may also be more prone to making impulsive financial decisions because of their emotional reactivity.

Extraversion

Extraverted individuals are outgoing, sociable, and assertive. Studies of this personality trait have yielded mixed results regarding debt accumulation, with some suggesting a positive correlation (possibly due to a desire for material possessions or social status) and other studies finding no significant relationship.

Type vs. Trait

Personality types and traits both aim to describe human behavior, but they do so in fundamentally different ways.

Personality types refer to the classification of individuals into distinct categories based on specific patterns of behavior, thought, and emotion. Types are often seen as qualitative categories; you either fit into a type or you don’t. They provide a broad framework for understanding motivations and behaviors.

Personality traits, on the other hand, are enduring characteristics or qualities that reflect consistent patterns in an individual’s thoughts, feelings, and behaviors. Traits are typically measured on a continuum, such as the Big Five personality traits.

In other words, types are categorical (e.g., introvert vs. extrovert), while traits occur on a spectrum (e.g., varying levels of extraversion).

Source: Personality Types

Debt Personalities

In addition to the Big Five personality traits, financial psychologists have identified distinct personality types with respect to how consumers manage and perceive debt. (See sidebar, “Type vs. Trait.”)

Let’s take a look at the five most common “debt personalities” recognized by financial behavior experts:

#1. The Avoider

This personality type avoids confronting financial issues, particularly debt. Avoiders may feel overwhelmed by finances and neglect to open bills or check account balances. This person also tends to procrastinate making debt payments or even acknowledging the amount owed.

The avoider’s anxiety about money often stems from childhood experiences or a lack of financial education. On some level, they believe that ignoring debt will make the problem go away.

#2. The Compulsive Spender

Compulsive spenders are conspicuous consumers, often buying things they don’t need. They’ll frequently use credit cards or arrange loans without considering long-term consequences. This personality type justifies debt as a way to “live in the moment” or “treat oneself.”

The compulsive spender’s unrestrained purchasing may be a reaction to stress or low self-esteem, or simply cultural pressure to maintain a particular lifestyle.

#3. The Anxious Saver

Fearful of debt and financial insecurity, anxious savers tend to over-save and under-invest. They’re often unwilling to spend money, even on necessities or meaningful experiences, due to fear of debt accumulation.

Frequently, these individuals were raised in a financially unstable environment, or they experienced monetary hardship at some point. As a result, they developed a belief that spending money inevitably leads to financial disaster.

#4. The Rational Debtor

Rational debtors are every A/R professional’s dream. They approach debt with logic and a clear repayment plan, often incurring debt strategically for investment purposes or to advance their career goals. These consumers are disciplined about making their payments and managing interest rates. Financial education at some point in their lives has made them pragmatic about spending and borrowing.

#5. The Carefree Borrower

Debt is not a serious issue for carefree borrowers, who are usually unconcerned about paying it off quickly (if at all). They rely on minimum payments and/or frequent refinancing instead of creating a feasible repayment plan. “Mañana” is their mantra, as they assume the debt will be easy to repay at some future date.

These individuals may have a history of readily accessible credit or financial assistance, which can lead to an “optimism bias,” the belief that future income will resolve their current financial issues without any consequences.

Collection Challenges

Collecting from avoiders, compulsive spenders, and carefree borrowers is often challenging. Avoiders must be located through skip tracing, compulsive spenders often have numerous accounts in collections at the same time, and carefree borrowers need to understand the seriousness of defaulting on their obligations.

If your collections team is overwhelmed by the time and energy required to collect from these consumers, it’s time to call for reinforcements. The CBSI professionals have the required technology and training to ensure you’re paid what you’re due.

Sources:

Featured Image: Adobe, License Granted

FinTraits

True You Journal

Potentash

Social Science Research Network

Recent Posts

Share On: